AI Summary

About

Make (formerly Integromat) is a visual, no-code automation platform — an iPaaS — that lets users build “scenarios” connecting more than 3,000 apps with a drag-and-drop interface, and increasingly with AI agents and an MCP server. It targets a spectrum from individual prosumers automating personal workflows to SMB teams and large enterprises orchestrating critical business processes. The platform is owned by process-mining company Celonis (the pricing page footer reads ”© 2026 Celonis, Inc.”).

Make positions itself against Zapier and other automation tools on the strength of its visual-first builder, generous app library, and a usage-metered model that scales by volume rather than per-task seat counts. Active scenarios and users are unlimited on paid plans — what you buy is throughput, measured in credits.

The defining pricing fact for Make is that its value metric is the credit. Make renamed its long-standing “operations” metric to “credits”: for non-AI apps, one operation (a single module run) still equals exactly one credit, so the rename is a re-labeling of the metric rather than a repricing. AI features layer dynamic, token-based credit consumption on top of this base unit.

Pricing summary : how Make’s credit-metered automation pricing works

Make uses a credit-metered (volume-tiered) model with a free tier, structured around two dimensions:

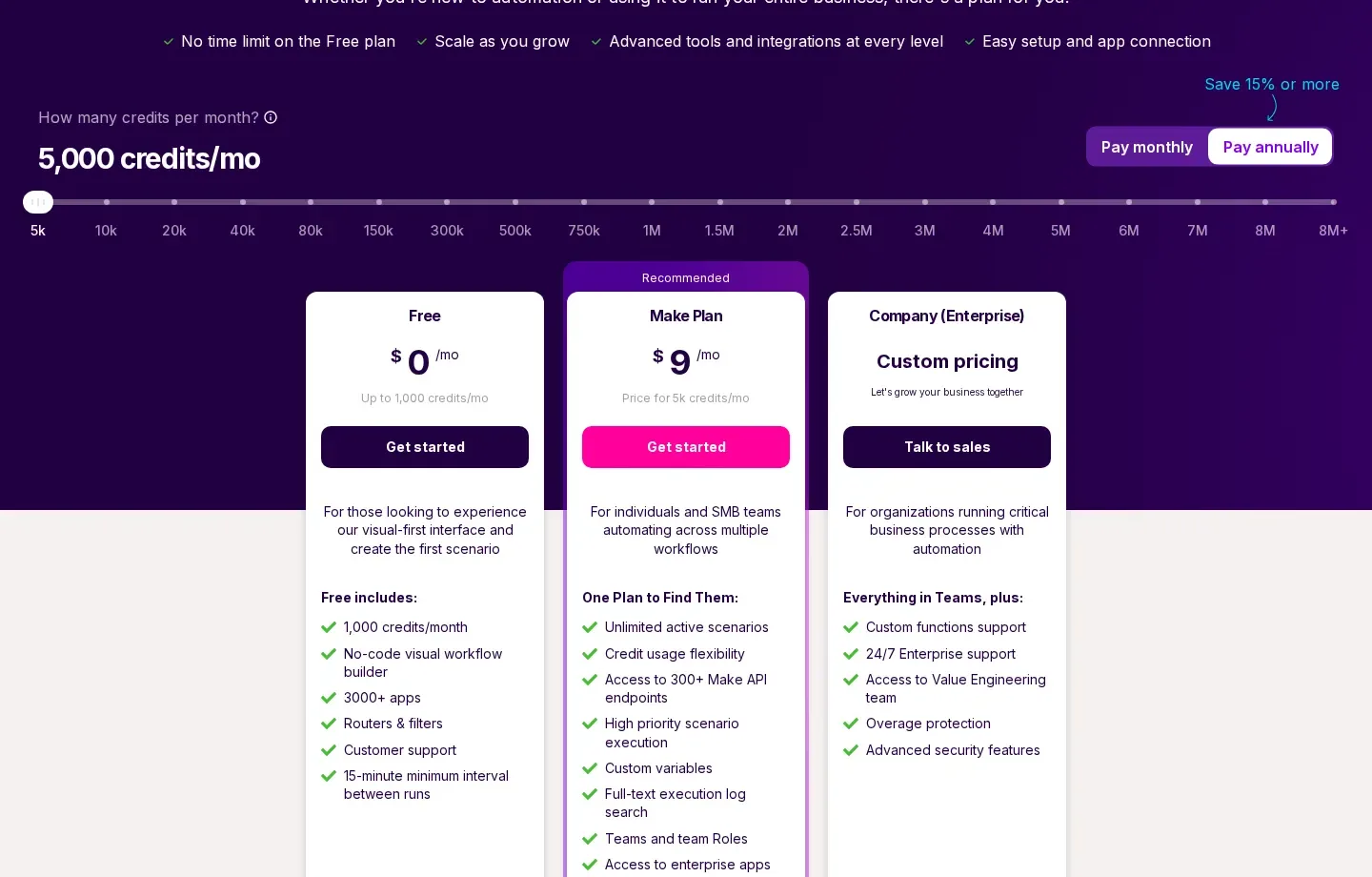

- Credit volume (the value metric): You buy a monthly credit allowance. For non-AI apps, 1 operation = 1 credit, where an operation is a single module run. The Free plan includes up to 1,000 credits/mo; the paid tiers (Core, Pro, Teams) all price on a shared slider that scales the monthly credit allowance from 10,000 credits/mo up to 8M+ credits/mo. At the entry 10k step, annual billing is $9/mo (Core), $16/mo (Pro), $29/mo (Teams); paying monthly costs about 17.6% more.

- Dynamic AI usage: AI and some advanced apps consume credits dynamically rather than 1:1. With Make’s AI Provider, credits are based on tokens and operations, with conversion rates that vary by model (e.g. GPT-5 mini at 1,500 tokens per credit; Claude Sonnet 4.5 at 301 input / 60 output tokens per credit). The Make Code App consumes 2 credits per 1 second of code-execution time.

What makes this different: Make sells throughput, not seats — active scenarios are unlimited on every paid tier, and all three paid tiers price on one shared credit-volume slider, so the feature tier and the throughput dimension are chosen independently.

Pricing by product

Make platform (Individual and SMB plans)

All paid prices below are the annual-billing rate at the entry 10,000-credit slider step; paying monthly costs about 17.6% more (Core ~$10.59, Pro ~$18.82, Teams ~$34.12 per month).

| Tier | Price (annual) | Included | Key mechanics |

|---|---|---|---|

| Free | $0 / mo | Up to 1,000 credits/mo, no-code builder, 3,000+ apps, routers & filters, 2 active scenarios | No time limit; 15-min minimum interval between runs |

| Core | from $9 / mo | 10,000 credits/mo at the entry step (up to 8M+); unlimited active scenarios, Make API, 1-min interval | ”Recommended” tier; price scales on the shared credit slider |

| Pro | from $16 / mo | 10,000 credits/mo entry; everything in Core plus priority execution, custom variables, full-text log search | Higher per-step price than Core at the same credit volume |

| Teams | from $29 / mo | 10,000 credits/mo entry; everything in Pro plus teams & team roles, shared scenario templates | Adds collaboration/governance on top of Pro |

Make platform (Enterprise)

| Tier | Price | Included | Key mechanics |

|---|---|---|---|

| Company (Enterprise) | Custom pricing | Everything in Teams, plus custom functions, 24/7 support, Value Engineering, SSO, audit logs, credit overage protection | Sales-led, quoted (“Talk to sales”) |

Sales motions across products: PLG / self-serve for the Free, Core, Pro, and Teams tiers (sign up online, slider-driven checkout); sales-led for the Company (Enterprise) plan.

Credit value-metric: how credits are consumed

The credit is Make’s single billing unit, replacing the older “operations” term. How a feature consumes credits depends on its type:

| Usage type | What drives credit consumption | Example |

|---|---|---|

| Fixed (non-AI apps) | A set rate per run; 1 operation = 1 credit by default, regardless of input/data size | Google Drive > Upload a File = 1 credit per upload |

| Fixed (some AI/extract) | A higher fixed rate per operation for processing-heavy modules | Some AI Content Extractor modules consume 2 or 10 credits per operation |

| Dynamic — tokens | Token volume (input + output) and model selected | GPT-5 mini: 1,500 tokens/credit; Claude Sonnet 4.5: 301 in / 60 out per credit |

| Dynamic — other | File size, page count, or processing time | Make Code App: 2 credits per 1 sec of code-execution time |

For third-party AI apps with a custom connection (e.g. OpenAI, Anthropic, Gemini), you pay Make for credits based on operations and your AI provider for tokens directly. With Make’s AI Provider (available on all plans), Make handles the AI connection and charges credits based on both tokens and operations.

Hidden costs : what real Make users actually pay as volume scales

The “from $9/mo” headline is Core’s annual rate at the entry 10,000-credit slider step, and it understates what an active account pays for three reasons: paying monthly rather than annually adds ~17.6% (Core ~$10.59/mo), non-AI scenarios spend credits on every module run, so a multi-step workflow burns several credits per execution, and AI modules abandon the clean 1-op-1-credit rate for dynamic, token-based consumption that scales with prompt and response size. Two archetypes show how the bill actually grows.

Archetype 1 — a non-AI scenario fans out across modules. For non-AI apps the rule is simple (1 module run = 1 credit), but a useful scenario rarely has one module. A trigger that routes through a filter, two app actions, and a logger consumes a credit per app module on every run:

| Line item | Credits/mo |

|---|---|

| A 4-module scenario (trigger → 3 external-app actions), run 5,000×/mo | ~20,000 |

| A second 3-module scenario run 4,000×/mo | ~12,000 |

| Monthly total | ~32,000 credits — past the 20k slider step, into the 40k tier |

Because the Make Plan price scales on the credit slider, a couple of moderately wide scenarios move an account several steps up (5k → 10k → 20k → 40k). The credit unit is finer and far cheaper than Zapier’s per-task meter — community consensus puts Make at roughly 5–7× cheaper than Zapier at the same volume — but the meter still ticks per module, not per scenario, so picking the right value metric to model against matters before you commit to a tier.

Archetype 2 — AI modules turn a flat meter into a variable one. This is where the August 2025 rename bites. With Make’s AI Provider, credits are consumed dynamically by tokens and model choice, so the same agent costs wildly different amounts depending on which model it calls and how much it reads and writes:

| AI usage (Make’s AI Provider) | Credit consumption | What 1M input tokens ≈ |

|---|---|---|

| GPT-5 mini (Make’s “Large” tier) | 1,500 tokens / credit | ~667 credits |

| Claude Sonnet 4.5 | 301 input / 60 output tokens / credit | ~3,300 input + 16,700 output credits |

| Make Code App | 2 credits / 1 sec of code-execution time | ~120 credits per minute of runtime |

An AI agent that reads a long document and replies on Sonnet 4.5 can consume thousands of credits in a single run — so a workflow that looked like “1 operation” under the old model now burns credits like an AI-agent cost monster. This is the core of the post-rename “bill shock” complaint: the headline metric stayed 1:1 for non-AI apps, but the AI modules people increasingly rely on consume a variable, harder-to-forecast number of credits. At very high volume (~50,000–100,000+ runs/mo) the math tips toward self-hosted n8n, whose per-execution model on a ~$5–6/mo VPS undercuts any credit meter.

Want to estimate your own Make bill? Use the Make pricing calculator to model your monthly cost based on credit volume and AI usage.

Pricing evolution : from Integromat operations to Make credits

Make’s pricing lineage runs from Integromat — a bootstrapped Prague startup priced per operation — through a Celonis acquisition and rebrand, to today’s credit-metered slider. Make publishes no Wayback-legible historical pricing snapshots for the make.com era, so the timeline below is anchored to dated company milestones (acquisition, rebrand, the operations → credits rename) and the live 2026 capture; dollar figures that were never independently legible are marked unknown rather than guessed.

Cadence

| Quarter | Price changes | Product / SKU additions | Notes |

|---|---|---|---|

| 2020 Q4 | 0 | 0 | 2020-10: Celonis acquires Integromat (reported $100M+). Pricing stays per-operation under the Integromat brand; no public change. |

| 2022 Q1 | unknown | 1 | 2022-02-22: Integromat rebrands to Make (make.com) as a semi-autonomous Celonis unit under CEO Fabian Q. Veit. Per-operation metric carried over; entry-tier dollar figures not independently legible (unknown). |

| 2025 Q3 | 0 | 1 | 2025-08-27: “operations” renamed to credits (1:1 for non-AI apps); AI modules move to dynamic, token/file/page/run-time credit consumption. Make states plan pricing and limits were unchanged — a metric rename, not a repricing. |

| 2026 Q2 | 0 | 3 | Capture 2026-06-11: Make replaced the single “Make Plan” with a tier ladder — Free ($0), Core ($9/mo), Pro ($16/mo), Teams ($29/mo) at the 10,000-credit entry step (up from a 5,000-credit single plan on 2026-06-02), Company/Enterprise (custom). Annual billing saves 15%+; monthly billing adds ~17.6%. |

Tracked range: 2020-10 – 2026-06. “unknown” price-change cells mark quarters where a brand or structural change is dated and verifiable but the underlying dollar figures never rendered in an archive and are not independently legible — they are not guessed.

Notable changes

- 2020-10 — Celonis acquires Integromat (Make’s predecessor) for a reported $100M+; the platform keeps its per-operation pricing under the Integromat name.

- 2022-02-22 — Integromat rebrands to Make (make.com), relaunched as a semi-autonomous business unit inside Celonis led by Founder/CEO Fabian Q. Veit. (Make blog.)

- 2025-08-27 — Make renamed its billing unit from “operations” to “credits”; for non-AI apps 1 operation continues to equal 1 credit, while AI apps move to dynamic, token-based credit consumption. (Make Help Center — Credits.)

- 2026-06-02 — Single “Make Plan” tier: Free / Make Plan (from $9/mo, 5,000-credit slider step up to 8M+) / Company (Enterprise, custom); annual billing saves 15%+.

- 2026-06-11 — Make restored a paid tier ladder — Free / Core ($9/mo) / Pro ($16/mo) / Teams ($29/mo) at a 10,000-credit entry step (up from 5,000) / Company (Enterprise, custom). All three paid tiers price on one shared credit slider; monthly billing runs ~17.6% above the annual rates ($10.59 / $18.82 / $34.12). (Make pricing page.)

What’s unique : credit-as-metric and the volume slider

1. One shared credit-volume slider prices every paid tier. Make’s three paid tiers (Core, Pro, Teams) don’t each carry their own price ladder — a single “How many credits per month?” slider, stepping from 10,000 to 8M+, sets the price for all of them at once, and choosing Core/Pro/Teams layers feature access on top. (For most of early 2026 Make went further and collapsed the paid offering into a single “Make Plan”; by mid-2026 it had restored the named tiers while keeping the shared slider.) The buying decision stays close to one dimension — throughput — with a light feature-tier choice on top and deep feature gating reserved for Enterprise.

2. Throughput is priced, seats and scenarios are free. On the paid Make Plan, active scenarios and users are unlimited; what you buy is credits. This decouples the bill from headcount entirely — the opposite of seat-based SaaS — and means a 2-person team and a 200-person team running the same volume pay the same. It is a deliberate bet that usage-based expansion beats per-seat revenue.

3. A metric rename that quietly changed the math for AI users. The August 2025 “operations → credits” switch kept a strict 1:1 mapping for non-AI apps, so Make could honestly say plan pricing was unchanged. But it simultaneously moved AI modules onto dynamic consumption — tokens, file size, pages, run time — so the same abstract unit now meters two very different kinds of work. Renaming the unit to “credits” gave Make a single currency flexible enough to absorb variable AI cost, at the price of a less predictable bill for AI-heavy users.

4. Dynamic per-model credit conversion bakes the LLM cost curve into the meter. Under Make’s AI Provider, each model has its own token-to-credit rate (GPT-5 mini at 1,500 tokens/credit; Claude Sonnet 4.5 at 301 input / 60 output per credit), so the meter passes the underlying model economics straight through to the customer. This sidesteps the value-metric problem for Make’s margin — credits track real provider cost — but pushes forecasting complexity onto the buyer.

5. The visual-first middle ground between easy-but-pricey and cheap-but-technical. Make’s strategic position is explicit: more visual and approachable than self-hosted n8n, and materially cheaper per unit than Zapier (community consensus puts it ~5–7× below Zapier at equivalent volume). Its credit unit is finer-grained than Zapier’s per-task meter, which is what lets it occupy that price-and-usability middle.

Strengths & weaknesses

| Strengths | Weaknesses |

|---|---|

| Finer, cheaper unit than Zapier — ~5–7× cheaper at equivalent volume | Per-module (not per-scenario) metering: wide workflows burn many credits |

| Single credit slider keeps the buying decision to one dimension | AI modules’ dynamic credit consumption makes bills hard to forecast |

| Unlimited scenarios and users on the paid plan remove seat friction | ”Operations → credits” rename raised effective AI costs and drew bill-shock complaints |

| Visual-first builder is more approachable than self-hosted n8n | At very high volume, self-hosted n8n (~$5–6/mo VPS) is far cheaper |

| 3,000+ apps plus native AI agents, MCP server, and AI Toolkit | Enterprise pricing is fully opaque (“Talk to sales”) |

| Generous free tier (1,000 credits/mo, no time limit) lowers the on-ramp | Credit is an abstract unit — less intuitive than a “task” or “run” |

Billing UX : the credit slider, billing toggle and overage controls

- Credit-volume slider — “How many credits per month?” sets each paid tier’s price directly, stepping from 10,000 credits/mo up to 8M+ (10k, 20k, 40k, 80k, 150k, 300k, 500k, 750k, 1M, 1.5M, 2M … 8M+).

- Monthly / annual billing toggle — “Pay monthly” vs “Pay annually” with a “Save 15% or more” label, switching the displayed tier prices between monthly and annual billing (e.g. Core $10.59 monthly vs $9 annual per month).

- Credit usage flexibility with yearly billing — prepay annual credits that only expire after 12 months instead of each month (paid-plan benefit).

- Credits overage protection — uninterrupted scenario execution once the credit limit is reached (Enterprise plan).

- Buy extra credits / auto-purchase — if credits run out before the next cycle, users can upgrade, buy extra credits, or enable extra-credit auto-purchasing.

- Credits toggle on the scenario canvas — each module’s white bubble shows operation count (checkmark icon) and credits consumed (coin icon), toggled next to the scenario name.

Strategic wins : why Make’s metric choices worked

1. Undercutting Zapier on a finer, cheaper unit

Make’s per-operation (now per-credit) meter is granular and priced well below Zapier’s per-task model — roughly 5–7× cheaper at equivalent volume by community consensus. That price gap is Make’s primary wedge against the category leader: it concedes Zapier’s integration breadth and brand while winning the cost-sensitive automation buyer. Choosing a cheaper, finer value metric than the incumbent is a textbook challenger move, and it is worth comparing against the rest of the automation field in the pricing blueprint.

2. Selling throughput, not seats

By making active scenarios and users unlimited on the paid plan and pricing only credits, Make lets automation spread across an organization without per-seat procurement friction, then recovers value as usage grows. That is the land-and-expand logic of usage-based SaaS applied cleanly — the bill follows the work, not the org chart, which is exactly the usage-based packaging pattern that suits a tool meant to touch every department.

3. Pricing every tier on one shared slider

Pricing all three paid tiers on a single credit-volume slider turns the volume half of plan selection into a one-dimensional throughput choice: you pick a feature tier (Core/Pro/Teams), then a credit number, and see a price. It reduces decision friction at the point of purchase and makes self-serve checkout almost frictionless. It also future-proofs the model on the capacity axis — new throughput is just another slider step, not a new SKU to design and market — even as Make has oscillated between a single “Make Plan” and a named-tier ladder on the feature axis.

4. Using “credits” as a single currency for mixed AI and non-AI work

Renaming “operations” to “credits” gave Make one abstract unit flexible enough to meter both flat non-AI runs (1:1) and variable, token-driven AI work in the same wallet. That lets Make pass per-model LLM economics straight through the meter without inventing a separate AI add-on the way Zapier did — a structurally simpler answer to the problem of pricing AI-agent workflows whose cost is a moving target.

Areas to improve : gaps and proposed fixes

1. Make AI credit consumption predictable before the run

The biggest post-rename complaint is that AI modules consume a variable, hard-to-forecast number of credits — the same workflow can cost wildly different amounts depending on model and payload. A pre-run estimate (“this run will cost ~X credits at current model rates”), per-model cost previews in the module builder, and budget caps on AI scenarios would defuse the bill-shock pattern that variable AI metering creates. The canvas already shows credits consumed after a run; showing the projected cost before is the missing half.

2. Add spend alerts and circuit-breakers on credit burn

Make offers extra-credit auto-purchasing and Enterprise overage protection, but a self-serve account can quietly accelerate its credit burn — especially via AI modules — without an early warning. Approaching-limit alerts, a configurable hard cap, and an anomaly circuit-breaker on a runaway scenario are the thresholding and alerting controls usage-priced vendors are now expected to ship, and they would convert “buy more credits” from a surprise into a deliberate choice.

3. Publish per-step slider prices and an Enterprise band

Only the entry 10k-credit step is shown as a headline (Core $9, Pro $16, Teams $29 annual); the price at 80k, 300k, or 1M credits appears only as you drag the slider, and Enterprise is fully “Talk to sales.” Surfacing the full per-step price ladder (or indicative bands) and an entry Enterprise range would let buyers model real cost before committing — the transparency the better usage-invoicing playbooks call for, and a low-friction way to shorten the procurement conversation.

Monetization stack & signals : how Make builds & buys its revenue engine

Buys 4 Builds 1 1 signal role

Make sells a public self-serve credit-slider checkout, yet it is building a full "AI-led revenue operations engine" on bought GTM tooling — Salesforce CRM, Snowflake, and Clay. The signal worth watching is the GTM Engineer below: a sales-led enterprise motion being engineered on top of the self-serve credit core.

- Credit metering Metering inferred

-

“Full ownership of the data enrichment lifecycle within Salesforce and Snowflake … ensure Salesforce remains reliable for reporting and analytics.”

-

“Maintain an organized book of business and consistently track engagement using CRM tools like Salesforce and HubSpot.”

-

“Full ownership of the data enrichment lifecycle within Salesforce and Snowflake. You will architect and maintain end-to-end pipelines.”

-

“someone who thinks in systems, builds in Clay and Make … architect and maintain end-to-end pipelines, utilizing Clay and AI, while managing campaign operations, credit budgeting.”

-

A self-serve, credit-metered platform staffing a dedicated Revenue Programs GTM Engineer to architect an "AI-led revenue operations engine" on Salesforce + Snowflake + Clay — the canonical sales-led enterprise motion being engineered onto a PLG self-serve core, built largely with Make's own automation product.

“build a world-class, AI-led revenue operations engine … You will own the AI and automation infrastructure that powers our entire GTM motion — from end-to-end data enrichment pipelines … to sales coaching agents, forecasting tools.”

Signals reviewed · derived from public job posts

Job postings fill and close over time — once a posting is filled we keep it as a dated citation (the quoted evidence remains); use View open roles for current listings.

Key takeaways

- A finer, cheaper unit can be a wedge against the incumbent. Make’s per-credit meter is granular and ~5–7× cheaper than Zapier’s per-task model at volume, and that price gap — not feature parity — is its primary way of winning the cost-sensitive automation buyer.

- Pricing every tier on one slider reduces purchase friction. By pricing all three paid tiers on a single shared credit-volume slider, Make turns the volume half of plan selection into a one-dimensional throughput choice and makes self-serve checkout almost frictionless — you pick a feature tier, then a credit number, and see a price.

- A metric rename is never just cosmetic. Renaming “operations” to “credits” let Make truthfully say plan pricing was unchanged while simultaneously moving AI work onto dynamic consumption — proof that the unit you bill in shapes the bill even when the headline number holds.

- Pricing seats out of the model is a growth bet. Unlimited scenarios and users on the paid plan remove procurement friction and let automation spread org-wide, with value recovered on the credit dimension as usage grows.

- Abstract units trade intuition for flexibility. “Credits” is flexible enough to meter both flat non-AI runs and variable AI work in one wallet, but it is less intuitive than a “task” or a “run,” which is why predictability tooling (estimates, alerts, caps) becomes essential rather than optional.

UBP implications

- One abstract unit can absorb mixed workloads — at a forecasting cost. A credit that maps 1:1 for non-AI runs but flexes dynamically for AI work lets a vendor price two very different kinds of usage in a single currency, but it shifts forecasting burden onto the buyer and demands strong pre-run visibility.

- Dynamic, pass-through metering protects margin but moves the value-metric problem downstream. Tying credits to per-model token rates keeps the vendor’s margin aligned with real provider cost; the unpredictability that creates for customers is the recurring tension in pricing AI-era usage.

- A shared volume slider can price a whole lineup. Letting one credit-volume control set the price for every paid tier shows that usage-based pricing can keep plan selection close to a single dimension — provided the per-step price ladder is transparent enough for buyers to model before they commit. Make’s flip-flop between a single “Make Plan” and a named-tier ladder underlines that the feature axis and the volume axis are separable design choices.

Sources

- Make pricing page (accessed 2026-06-11)

- Make AI Agents (accessed 2026-06-11)

- Make Help Center — Credits (accessed 2026-06-11)

- Make Help Center — Operations (accessed 2026-06-11)

- Make Enterprise plan (accessed 2026-06-11)

- Compare other automation pricing in the pricing blueprint

Bottom line

Make sells automation throughput by the credit: for non-AI apps the metric is dead simple (1 operation = 1 credit), the paid tiers (Core, Pro, Teams) all price on one shared credit-volume slider from $9/mo (annual), and AI usage layers dynamic, token-based credit burn on top — a clean, scale-with-usage model wrapped around an unlimited-scenarios promise.

Want to compare Make against other automation and usage-based pricing? Browse the pricing blueprint.

Pricing timeline : Major events on a vertical axis

Each milestone below corresponds to a public pricing change, product launch, or material adjustment. Major events use a filled marker; minor adjustments use a faded one.

Paid tier ladder restored; entry step moves to 10k credits

Make replaced the single 'Make Plan' with three named paid tiers priced at a 10,000-credit entry step — Core ($9/mo annual, $10.59 monthly), Pro ($16/mo annual, $18.82 monthly), and Teams ($29/mo annual, $34.12 monthly) — alongside Free ($0/mo) and Company/Enterprise (custom). The credit-volume slider now starts at 10,000 credits/mo (up from 5,000) and scales all paid tiers together up to 8M+. Annual billing still saves 15% or more.

Single 'Make Plan' slider tier

Free ($0/mo, up to 1,000 credits/mo), a single 'Make Plan' (from $9/mo at 5,000 credits/mo on a credit-volume slider), and Company/Enterprise (custom pricing). AI features billed via dynamic credit usage.

Operations renamed to credits

Make rebranded its core billing unit from 'operations' to 'credits'. For non-AI apps, 1 operation continues to equal 1 credit; AI apps can consume credits dynamically based on tokens, file size, pages, or run time. Make states existing plans and pricing remained unchanged.

Integromat rebrands to Make (make.com)

Integromat relaunched as Make, a semi-autonomous business unit inside Celonis, led by Founder/CEO Fabian Q. Veit (formerly Celonis COO). The rebrand carried over the per-operation value metric; the visual scenario builder and app library were preserved under the new make.com brand.

Celonis acquires Integromat (Make's predecessor)

Process-mining company Celonis acquired Integromat — a bootstrapped automation startup from Prague, Czech Republic — for a reported $100M+. Integromat continued operating under its own name while Celonis folded it into its product portfolio. No public pricing change accompanied the deal.

- · Make renamed its core billing unit from 'operations' to 'credits' — for non-AI apps 1 operation still equals exactly 1 credit, so the change is a rebrand of the metric, not a repricing.

- · Make's pricing page pairs a credit-volume slider (10,000 credits/mo up to 8M+) with four named tiers — Free, Core, Pro, and Teams — so at any slider step you still pick a feature tier; Core starts at $9/mo (annual) for 10k credits.

- · Make is owned by process-mining company Celonis (the pricing-page footer reads '© 2026 Celonis, Inc.').

Questions & answers

- What is a credit in Make?

- A credit is the unit Make charges for consuming the platform. For non-AI apps, one operation (a single module run) equals one credit. AI and some advanced apps use dynamic credit consumption based on tokens, file size, pages, or processing time.

- How much does Make cost?

- Make has a Free plan ($0/mo, up to 1,000 credits/mo) and three paid tiers priced at a 10,000-credit entry step on annual billing — Core ($9/mo), Pro ($16/mo), and Teams ($29/mo) — each scaling up via a shared credit-volume slider, plus a Company/Enterprise plan with custom pricing. Paying monthly instead of annually costs about 17.6% more (Core ~$10.59/mo).

- What is the difference between credits and operations in Make?

- Operations show the outcome of activity on the platform (each module run is an operation), while credits are the currency you buy and consume. For non-AI apps the two are 1:1; AI usage can make credit consumption diverge from raw operation counts.

- How are AI features billed in Make?

- AI features use dynamic credit usage. With Make's AI Provider, credits are based on tokens and operations, with per-model conversion rates (e.g. GPT-5 mini at 1,500 tokens per credit). With a custom AI provider connection you pay Make for operations-based credits and your AI provider for tokens directly.

- Is Make cheaper than Zapier?

- At equivalent volume, Make is widely reported to be roughly 5-7x cheaper than Zapier, because Make's credit unit is finer-grained and priced lower than Zapier's per-task meter. Self-hosted n8n is cheaper still at high volume (a $5-6/mo VPS running unmetered executions), with the cost crossover where teams leave Make for n8n typically around 50,000-100,000 runs per month.